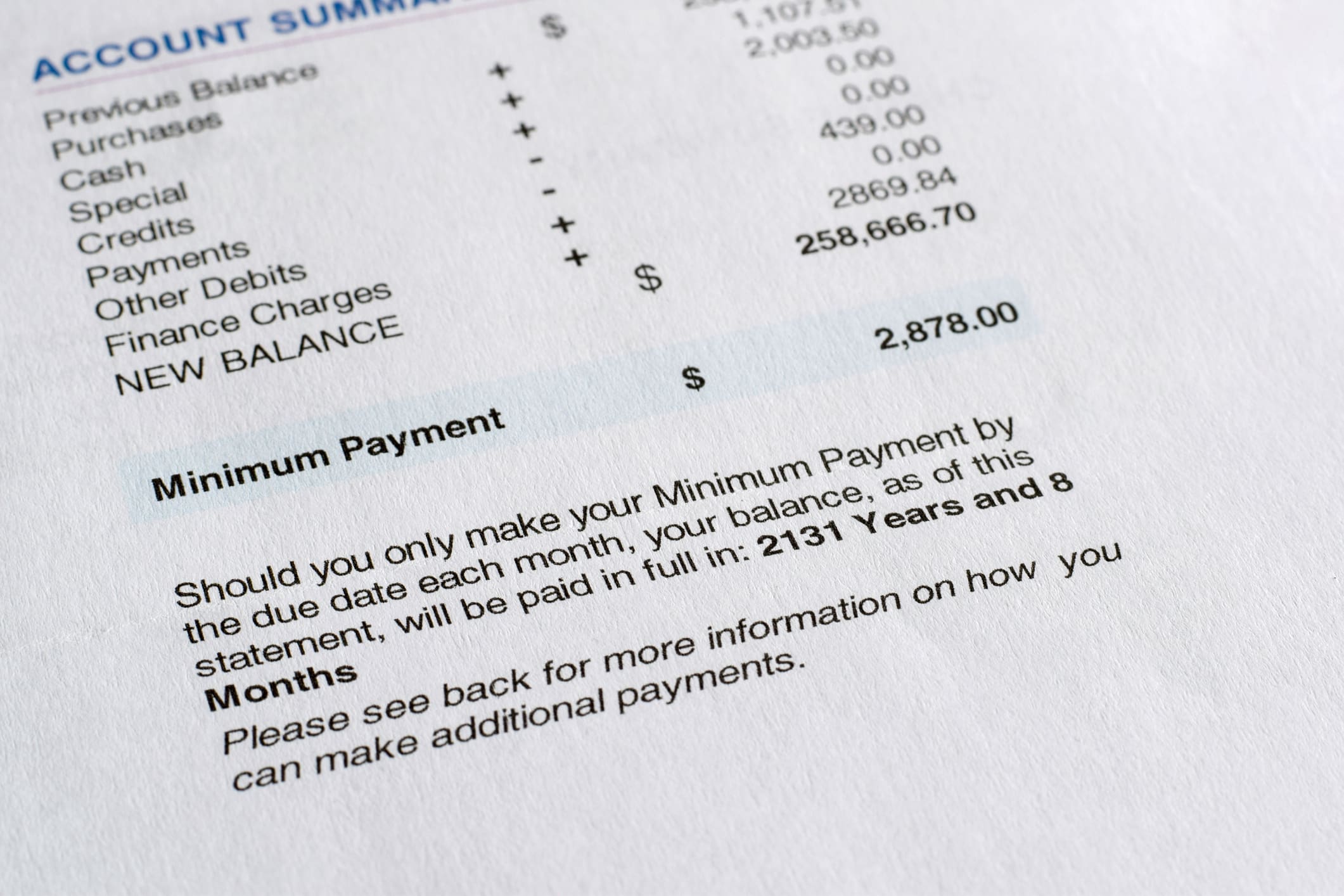

As we close out the first month of a new year, it’s a good time to check in on your personal debt situation and take steps to manage your high-interest debt.

Many Americans are charging like it’s 2019 again – before Covid – pulling out the plastic or typing in their digits to cover costs with credit cards. With sharp increases in credit card use and new auto loans, U.S. households saw their total debt increase by the largest margin in 15 years during the third quarter of 2022, according to a report from the Federal Reserve’s Consumer Credit Panel.

On a macro level, U.S. household debt – which includes home loans, revolving credit, student loans, and auto loans and leases – jumped by $351 billion (some 2.2%) to $16.51 trillion during that time period. According to the Federal Reserve, the balances Americans owe now stand $2.36 trillion higher, than at the end of 2019, before the pandemic and economic stimulus payments helped to cushion checking and savings accounts.

Not all debt is bad, of course. Home loans help us build equity for the future. But high-interest debt from credit cards and other loans should be reviewed regularly to see what can be tweaked to pay down that debt as quickly as possible. Here are some strategies to help manage your debt this year:

DIY Debt Consolidation

You may be able to consolidate several credit card debts using a balance transfer, Home Equity Loan, or Home Equity Line of Credit (HELOC). Then, you can take the new, cheaper loan, and use it to pay off credit cards, auto loans, and other debts with higher interest rates. By doing this, you could potentially cut how much you spend each month by hundreds or thousands.

Balance Transfers

You’ve likely heard of a balance transfer, which is when you move debt from one (or several) credit cards to another card with a lower interest rate. Your credit score comes into play here. The highest scores will help you qualify for cards with very low or 0% APR. Remember, though, the super-low rate will end after a certain period, usually 12 to 18 months. Also, when you get a balance transfer card, it’s wise to only use it for what was intended. That means avoiding new purchases. Tuck the card in a drawer or a safe to help avoid the temptation to use it.

Home Equity Loans

This is a fixed-rate loan, where you take out money and then begin paying it back immediately. This can be a good option for people with a large chunk of equity in their homes.

Pro-tip: Shop around for this type of loan as credit unions and online lenders often have the best rates.

Home Equity Line of Credit (HELOC)

This is a variable-rate loan that’s often tied to the prime interest rate. Because of that tie-in, if interest rates rise, so will monthly payments. One thing people like about taking out a HELOC is that the funds can be withdrawn as needed, instead of being required to take all the money at once. Typically, you pay back the money you take out, and are only charged interest on the funds you use. As with Home Equity Loans, they can be difficult to qualify for without substantial equity in your home. Shop around for the best interest rates on this loan, too.

Understand the Risks

Before consolidating – especially if you are rolling credit card debt into any type of home equity loan — remember you are essentially taking unsecured debt and turning it into a secure debt. That means if you default – you are unable to make your payments – the lender can take the asset associated with the loan, which, in this case, would be your home.