Do one thing: If you are late paying your bills, it’s time to cut spending on non-essentials and focus on spending only for necessities such as groceries, rent, utilities, and transportation for work.

More Debt Can Lead to Missed Payments

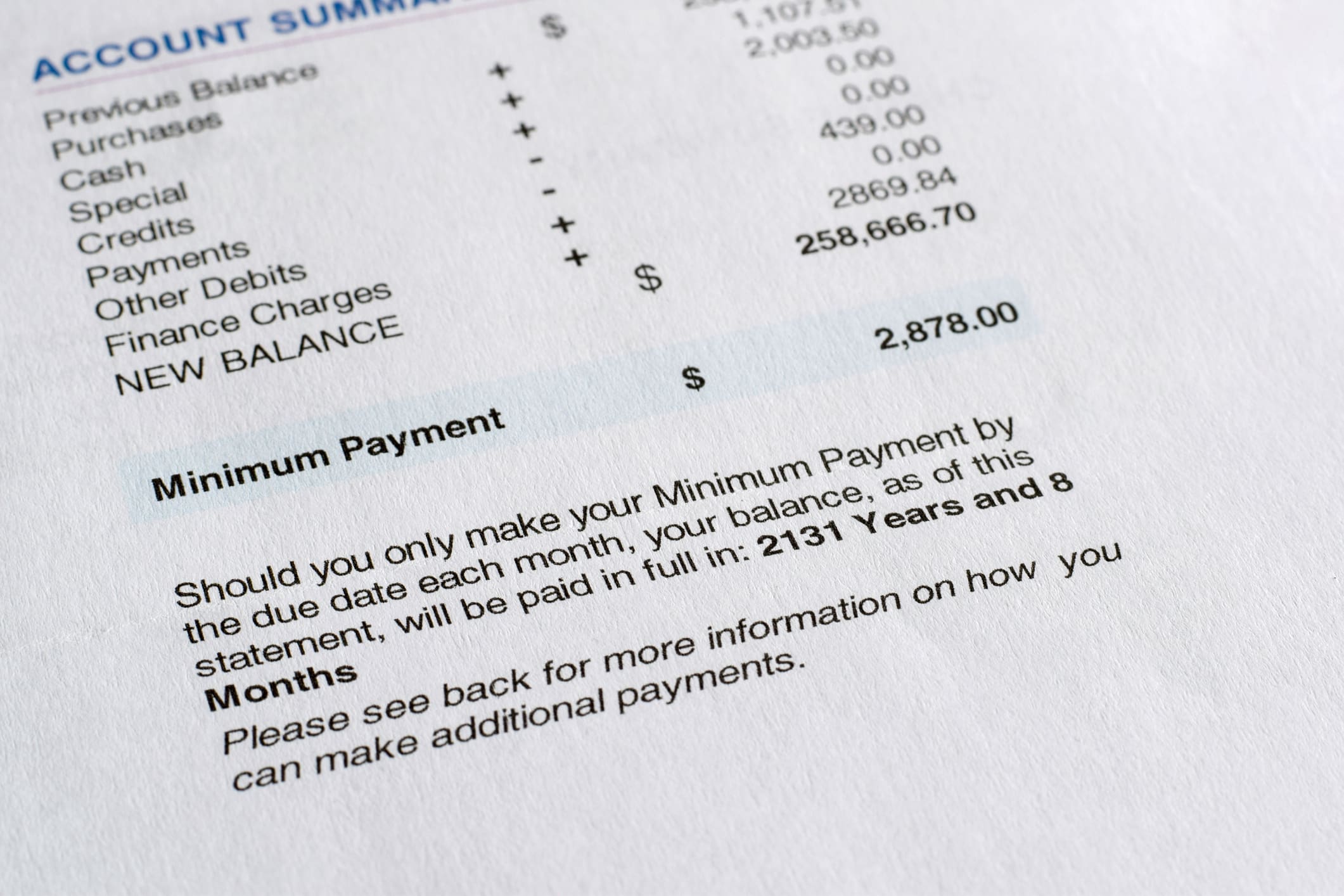

Americans are reaching for their credit cards more often, paying for everything from food to fuel as they wait for the next direct deposit to hit their accounts. Charging necessities – and everything else – can sometimes have unintended consequences. Credit card balances for U.S. adults rose to new heights at the end of 2025, growing by some $44 billion to $1.28 trillion, according to a January report by the Federal Reserve Bank of New York.

Personal Debt is Rising

As personal debt mounts, not everyone can adequately cover all their rising bills. The Federal Reserve’s monthly Survey of Consumer Expectations of about 1,200 adults, released in February 2026, also showed that fewer U.S. heads of households anticipate their financial situations will be better off a year from now.

Strategies for Seeking Help

For those who find themselves behind on payments, or who think they will be behind on payments in the coming months, there are steps you can take, including talking with creditors to explain your situation and work to find options that may be available, including what’s known as goodwill options or payment plans.

Call Your Creditors

If you can’t make payments, please don’t make the mistake of ignoring your creditors and lenders. You need to take a deep breath, set aside your pride, and make the call. It can’t hurt, and it could very well help the situation. Recent research shows that you have a good chance of getting a positive result. According to a June 2025 survey:

- 83%, or more than 4 in 5 account holders, who requested a lower interest rate on a credit card in the past 12 months had their request approved.

- That success rate was the highest the survey recorded since 2021.

- Other requests, such as increasing a credit limit or waiving an annual fee or late fee, were also more likely to be approved compared to previous years.

What Can You Ask For?

- Lower interest rates: When calling your credit card company, mention lower-rate offers from competitors, and ask them to match or reduce your current annual percentage rate (APR).

- Hardship programs: If you are struggling, ask about forbearance or a modified repayment plan that fits your budget.

- Potential settlements: You don’t always need to pay a third party to negotiate for you. You can settle debts or adjust terms yourself for free by keeping meticulous records of your conversations.

When You Call Creditors…

If you’re ready to call your credit card issuer to ask about your options, consider these steps:

- Locate the phone number on your card or monthly statement.

- Make the call and ask for an agent.

- When you reach them, let them know what’s going on.

- This is when you can ask for a lower interest rate to save money.

- If you are far behind, you can ask to set up a payment plan to pay back the debt.

- If they don’t agree, ask to speak to a supervisor and make your case again.

- Before you end a call, ask for written proof of any potential agreements.

Once you have that proof in hand, you’ll need to save it until all payments have been made.

Tips for Documenting the Call

It’s smart to take notes throughout a phone call with a creditor or lender, so you are able to keep accurate records. Be sure to include in your notes:

- The name of the person you speak with

- The date and time

- What you and the lender agree to do

- Any follow-ups

More Options for Handling Debt

“If calling your creditors doesn’t pan out, other options can potentially help,” says Certified Financial Planner Chris Diodato, CFA, CMT, founder of WELLth Financial Planning. “If you’re really in over your head,” Diodato recommends credit counseling.

Credit Counseling

- Go to a non-profit credit counselor who can then work with the issuer to create a debt management plan

- These plans can extend payments and reduce interest rates

- Often comes at the cost of negative marks on a credit report and needing to close the cards used in the plan

Debt Consolidation Loan

Depending on your circumstances, you may also qualify for a debt consolidation loan. Credit counseling agencies may be able to assist in reducing your high interest rates. The National Foundation for Credit Counseling (www.nfcc.org/) is a good resource for finding a counselor where you live. You can also check with your financial institution for credit counseling options.

With reporting by Casandra Andrews