When you miss multiple payments in a row, your credit will take a big hit. Fortunately, there are ways to rebuild your score. Here is how to do it.

Stop Digging

If you’re serious about getting out of the hole of debt, the first thing you need to do is stop digging. In other words, stop any further late payments. Your previous late payments are in the past, and we help you deal with that later. But for now, make it a goal, starting today, to be on time with all payments moving forward. Consistent on-time payments show the credit bureaus and lenders you’re committed to behavioral change. This will get you oriented in the right direction so you can start rebuilding.

Find the Root Cause

Before you start rebuilding your credit, try to first identify what actions and behaviors led to its decline in the first place.

Spending Without a Budget

Without structure or knowing how much money is coming in and how much is going out, spending can slowly start exceed income. Credit cards fill in the spending gaps, and high interest compounds the problem, making it more and more difficult to stay current on debt payments.

How to Fix It

If this is something you’re dealing with, the good news is the fix is simple:

- Track Spending. Make a note of every dollar spent for a week to give you a true picture of how and where you spend. This will provide clarity when you create your budget.

- Visualization. Writing down every dollar spent, swiped, tapped, or clicked will provide more awareness of where your money is going.

- Visualization. Writing down every dollar spent, swiped, tapped, or clicked will provide more awareness of where your money is going.

- Create a Budget. Putting a budget into action will help you allocate your income to cover your expenses more efficiently.

- Income. Calculate all income sources from wages, commissions, earnings, interest, tips, etc.

- Expenses. Start breaking down your monthly expenses into needs and wants.

- Needs are the things that sustain your day-to-day life: housing, food, and transportation.

- Wants are the extras, things like entertainment, eating out, travel, etc.

- If your expenses exceed your income, you may need to cut back on some of the non-essential wants.

- Pay Down High-Interest Debt. With a budget in place, you’ll be able to see where you can cut back expenses and reallocate those funds to pay down the high-interest debt.

Impulse-Driven and Emotional Spending

Sometimes we swipe the credit card impulsively when we’re stressed, bored, or trying to fill an emotional need with “retail therapy” spending. More often than not, this is just a short-term fix, and then we’re left dealing with the high-interest debt payments.

The Remedy

For impulsive or emotional spenders, the fix is putting safeguards in place to help you separate emotions from financial decisions. Here’s how:

- Time-Based Rules. Impulsive spending is easy to do. Click, swipe, done, without really thinking through the need for this particular purchase. Being more thoughtful about purchases helps relieve impulsive spending.

- Wait 24-48 Hours. Many financial advisors and budgeting specialists recommend waiting 24-48 hours to think about a purchase. In that time, you’ll be able to weigh the pros and cons, needs and wants, and then make a thoughtful decision whether to buy or not.

- Remove Stored Cards. Online retailers, in an effort to make your life easier, allow you to store your card information so you don’t have to enter the card number each time. In just two clicks, you’re done. The way to prevent this is to remove your stored credit card information from your phone or app, to give you a few minutes to think about the purchase while you search for your card.

Rebuilding Using a Secured Card

Sometimes, when your credit takes a big hit, it can be difficult to get a credit card. If this is the case, consider a secured credit card.

- Get Secure. Open a secured credit card with your current financial institution or online. These require you to put down a deposit, and they’ll have a spending limit.

- Spend Wisely. With a proper budget in place, you have a better handle on your expenses and where you spend. Use your secured card for your needs-based spending.

- Pay On Time, Every Time. The key to a secured card is to use it, but also to pay it off in full every month.

- Report Good Behavior. Make sure you’re getting recognition for your positive credit behavior, spending, and paying on time. Most financial institutions will report secured card data to the credit bureaus, so ask before setting up your secured card.

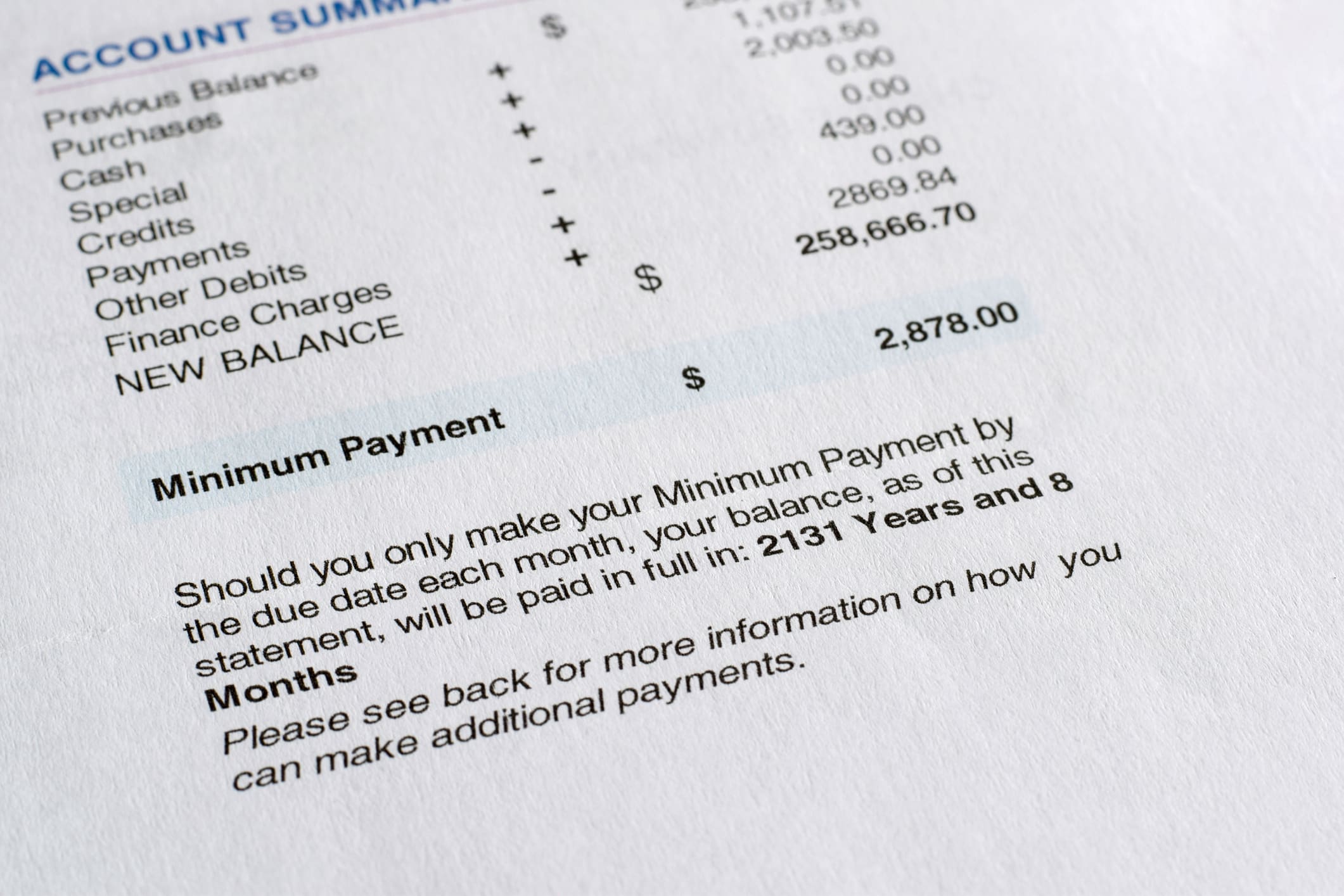

Keep Your Utilization Ratio Low

After payment history, which looks at whether you pay your bills on time, your credit utilization ratio is the second-most important factor in your credit score.

What is Credit Utilization?

Credit utilization is a credit bureau calculation that looks at the amount of credit you’re using compared to the credit limit. Here’s a breakdown of what that means:

- Credit Limit. This is the amount of credit you’re extended from a credit card issuer or financial institution. “You’re pre-approved for $3,000.” The credit limit is $3,000.

- Credit Usage. This is the amount of credit you’ve used. When you swiped your card for $500 at the tire shop, you used $500.

- Credit Utilization Ratio. While you may be extended $3,000 in credit, the credit bureaus lower your score the closer you get to that number. A good ratio is below 30% (or lower if possible). In this example, for a $3,000 credit limit, $900 credit usage is a 30% credit utilization ratio.

Do One Thing: Be patient and do the work. If you’re consistently on-time, keep your utilization in a healthy range, and stick to your budget, you’ll find your score will slowly rise once again.