You might have heard of debt consolidation loans as a way to simplify your finances and pay down multiple debts. You may have also wondered:

- What’s the difference between a personal loan and a debt consolidation loan?

- How do I know if either one is right for me?

Let’s clear that up and then get into how to actually choose the best option.

Head-to-Head Comparison

The difference between a debt consolidation loan and a personal loan is essentially nothing.

A “debt consolidation loan” isn’t a special type of loan. It’s just a personal loan used for a specific purpose—paying off other debts. Some lenders market them differently, but structurally, they work the same way.

So the real question isn’t which type of loan, but rather: Does using a personal loan to consolidate my debt actually improve my situation?

Personal Loan Basics

A personal loan is a type of installment loan that you repay in fixed monthly payments over a set period of time.

Typical features of Personal Loans:

- Loan amounts often range from $1,000 to $20,000 (or more)

- Fixed repayment term (e.g., 2–5 years)

- Usually, a fixed interest rate

- Funds can be used for almost anything, including paying off credit cards

When used for consolidation, you take out one loan and use it to pay off multiple existing debts.

Potential Benefits

If used strategically, consolidation with a personal loan can help:

- Lower interest rate. Credit cards often carry high rates. If the personal loan interest rate is significantly lower, more of your payment goes toward reducing the balance instead of to interest repayment.

- One monthly payment. Instead of trying to remember and keep track of multiple due dates and balances, you simplify everything into a single payment.

- Predictability. Most personal loans have fixed rates and terms, so your payment stays the same, and you have a clear payoff timeline.

A Word of Caution

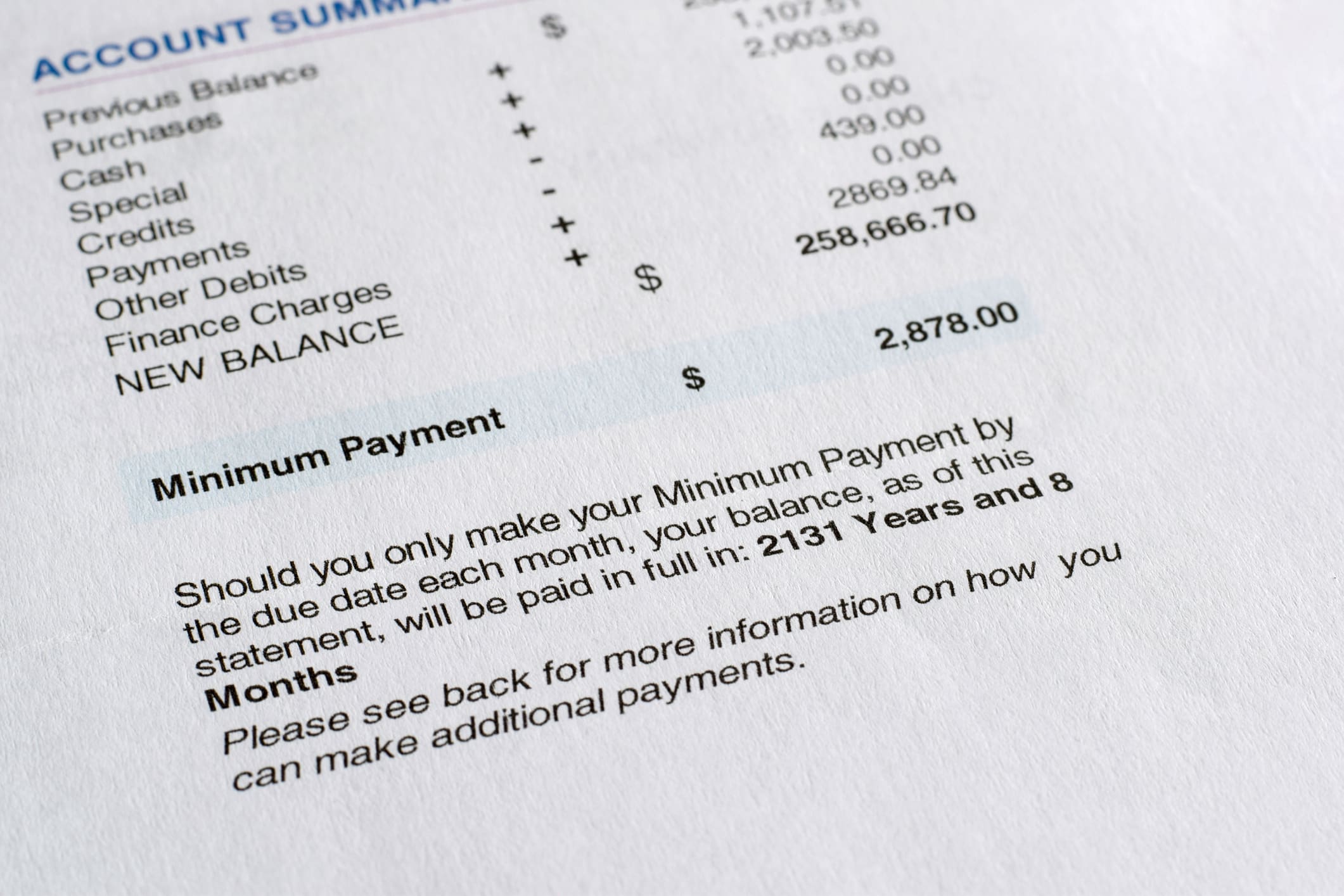

While a debt consolidation loan may seem like the answer to all your problems, there are some things to keep in mind. Many people make a faulty assumption that consolidation automatically solves the problem. It doesn’t.

A personal loan can make things worse if:

- The personal loan interest rate isn’t actually lower

- Fees are greater than the potential interest savings

- You continue using your credit cards after paying them off

- The repayment term is extended so that you pay more total interest in the long run

How to Determine the Best Option

Instead of focusing on labels, compare your options using the following criteria:

1. Compare Total Cost

A lower monthly payment can be misleading if it stretches the loan out longer. Be sure to examine these things as well:

- Interest rate (APR)

- Fees

- Total interest paid over time

2. Is the Rate Actually Better?

If you qualify for a lower rate than your current interest rates (especially credit cards), consolidation is more likely to help.

3. Consider Your Repayment Discipline

You know your spending behavior. Take an honest look at how you use credit cards. If you’re likely to use your cards and run balances back up after consolidating, you’re just layering debt. In that case, consolidation alone won’t fix the issue.

4. Look at Alternatives

A personal loan isn’t the only path available to you. Depending on your situation, you might consider:

- Balance transfer credit cards (low intro rates, but temporary)

- Debt management plans (structured repayment through a nonprofit)

- Accelerating repayment on existing debt

Each has trade-offs—especially around fees, timelines, and flexibility.

5. Match the Solution to Your Goal

Your financial goals can also be an important indicator of which consolidation option you choose.

- Simplicity. Consolidation may help.

- Cut Interest Costs. Compare all options carefully.

- Help with Payments. You may need a structured plan, not just a new loan.

Bottom Line

A debt consolidation loan is just a personal loan used strategically—but whether it’s a good idea depends entirely on the details. The best option is the one that:

- Lowers your total interest

- Shortens (or at least doesn’t extend) your payoff timeline

- Allows you to stick with the plan

Do One Thing: Before consolidating, calculate how much you’ll pay in total interest with the new loan versus your current debts—and commit yourself to not add new debt while you’re paying off the loan.