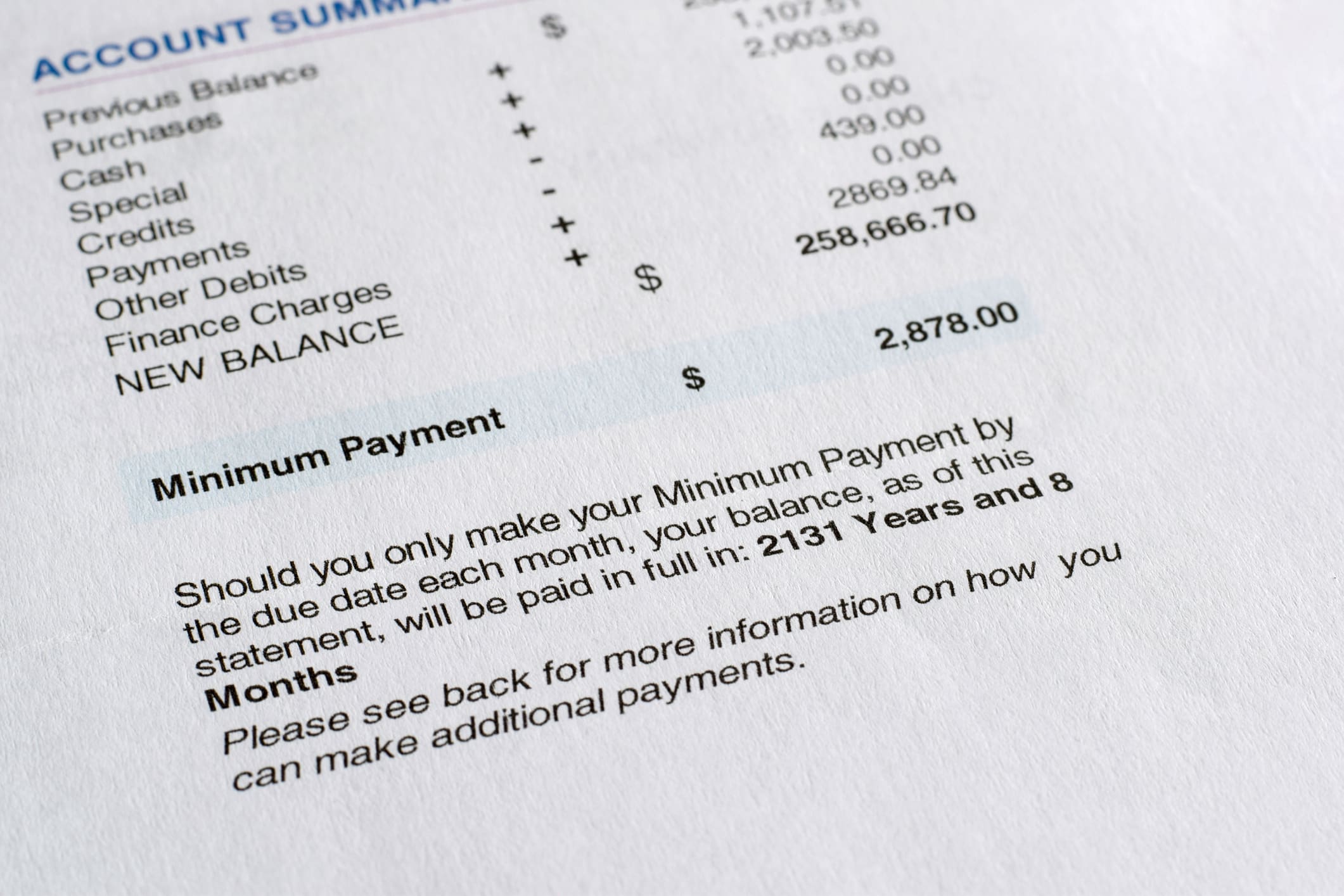

If you’re struggling with debt, you might want to consider debt consolidation as an option. The key, though, is to understand the pros and cons of this move before doing it. Here’s what you should know.

Pros of Debt Consolidation

- Lower Interest Rate. Perhaps the biggest selling point of debt consolidation is that you will likely get a lower interest rate. If you have a debt at a 25 percent interest rate, and open a consolidation loan with a 15 percent interest rate, not only will your monthly payment be lower, but you’ll save money on interest payments as well. Also, if you open a balance transfer credit card with a 0% intro interest rate, you’ll have a certain amount of time with zero percent interest to pay off your debt.

- Streamlined Payments. Consolidating your debt will make your life easier. Instead of having several bills a month, you’ll only have one monthly payment.

Cons of Debt Consolidation

- Qualification. To qualify for a debt consolidation loan or a balance transfer credit card, you’ll need decent credit. If you don’t have good credit, you’ll have a hard time finding a lower rate.

- Fees. Debt consolidation isn’t free. If you qualify for a consolidation loan, you’ll likely have some type of origination fee, usually between one and 10 percent of the total loan amount. Balance transfer cards also have fees. These will run you between three and five percent of the amount of debt you’re transferring.

Do One Thing: Make sure you can pay off your debt within the time frame of a debt consolidation loan or a balance transfer card’s initial offer.