Building or maintaining one credit score can feel daunting enough. But the truth is, most of us have dozens of slightly different scores out there that lenders use to decide whether to take a risk and loan us money, and how much interest we should pay.

What is a Credit Score?

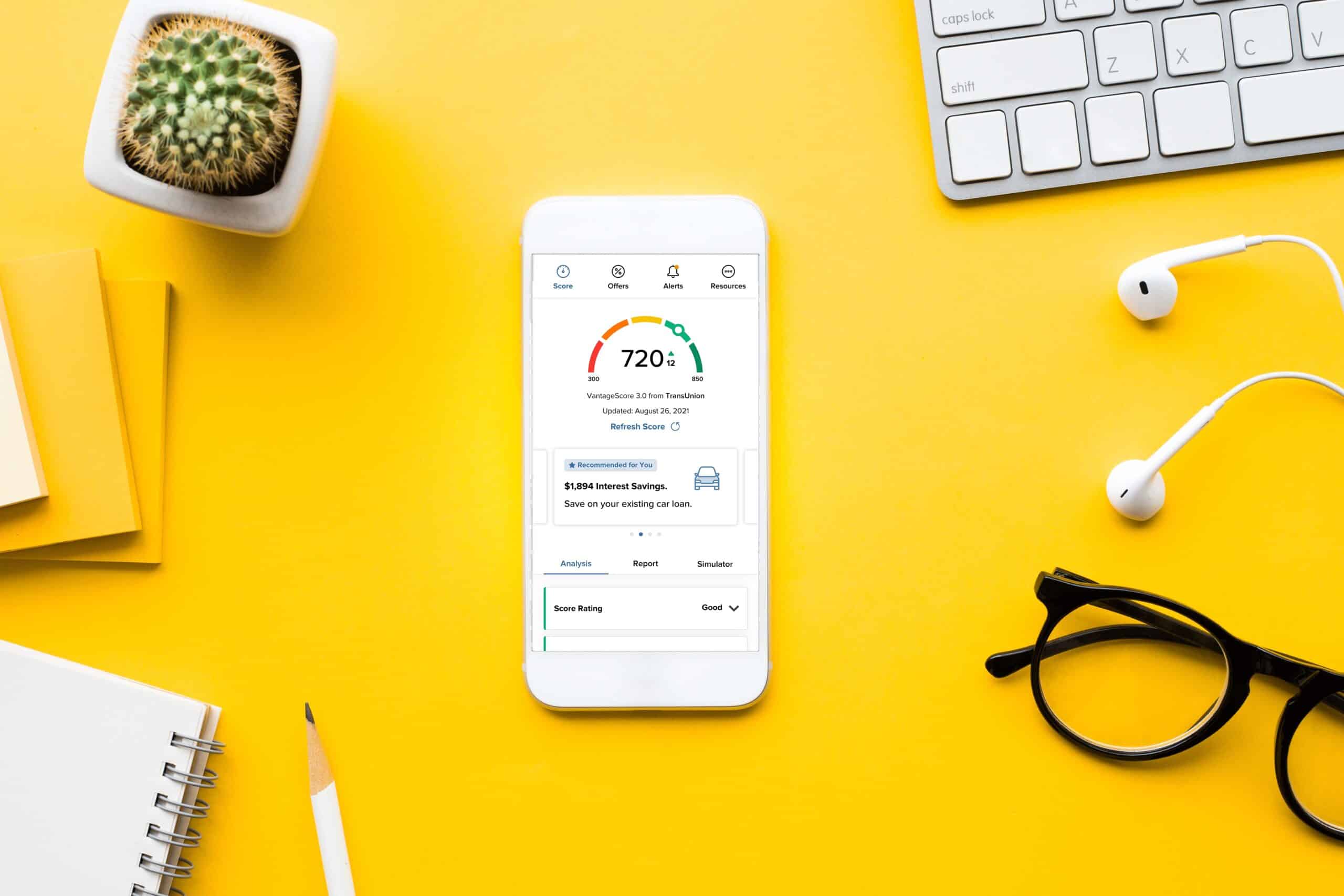

A credit score (which can range from 300 to 850) is like a report card that stays with us throughout our lives and reflects how we handle money.

How Credit Scores Are Defined

The three-digit number is typically defined by:

- The amount of debt you owe

- If your bills are paid on time

- The number of credit cards you have (and how long you have had them)

- If you have filed for bankruptcy in the last 10 years, among other factors

The Credit Bureaus

There are three major consumer credit reporting companies:

- Experian

- Equifax

- TransUnion

They collect information about you from financial institutions, your credit card issuers, and public records that are then used to determine your credit score.

Your Different Credit Scores

Credit scoring models rely on different mathematical formulas to analyze your credit history. Companies such as FICO® and VantageScore® create these models to help lenders assess credit risk. Beyond standard consumer scores, there are also industry-specific versions — including auto and credit card scores — that place different emphasis on factors like payment history, balances, or recent activity.

VantageScore vs. FICO: What’s the Difference?

Both models analyze similar categories — payment history, balances, credit age, types of credit, and recent activity — but:

- FICO® Scores are the most widely used by lenders, especially for mortgages. There are multiple FICO versions, and mortgage lenders often use older, industry-specific FICO models.

- VantageScore® was developed by the three major credit bureaus (Equifax, Experian, and TransUnion). It may weigh certain factors differently and can score consumers with shorter credit histories more easily than some FICO models.

Because the models use different formulas, your scores may vary slightly between them.

How Lenders View Your Scores

When you apply for a loan, a lender may pull one or multiple credit scores from one bureau or all three, and may use different scoring models depending on the loan type. You typically won’t know which score is used, and lenders aren’t required to disclose it — though you can ask.

- Trended Data. Newer models like VantageScore 4.0 use trended data, meaning they look at patterns over time — such as paying down debt or lowering balances — rather than just a single snapshot. Positive trends can help your score.

- Medical Debt. Unpaid medical collections generally aren’t reported until they’re at least six months old, giving you time to resolve billing issues before it affects your credit.

Keeping a Good Score

How can you best influence all of your credit scores? Here are some core principles that can help you build and maintain a good score:

- Pay your bills on time every single month

- Keep your balances low by using only 30% or less of what’s available to you

- Don’t apply for credit cards you don’t truly need

- Don’t close old accounts you no longer use unless they are charging fees.

You should also make sure to check your credit reports every few months to determine if there are errors that could be dragging down your scores. You have access to your scores for free on SavvyMoney through online or mobile banking.

With reporting by Casandra Andrews