When it comes to credit scores, there’s almost always room for improvement. If you’ve pulled your score and you’re not satisfied with the number you received, there are several strategies to boost it. But first, you need a little insight into how that score is calculated.

How is My Credit Score Generated?

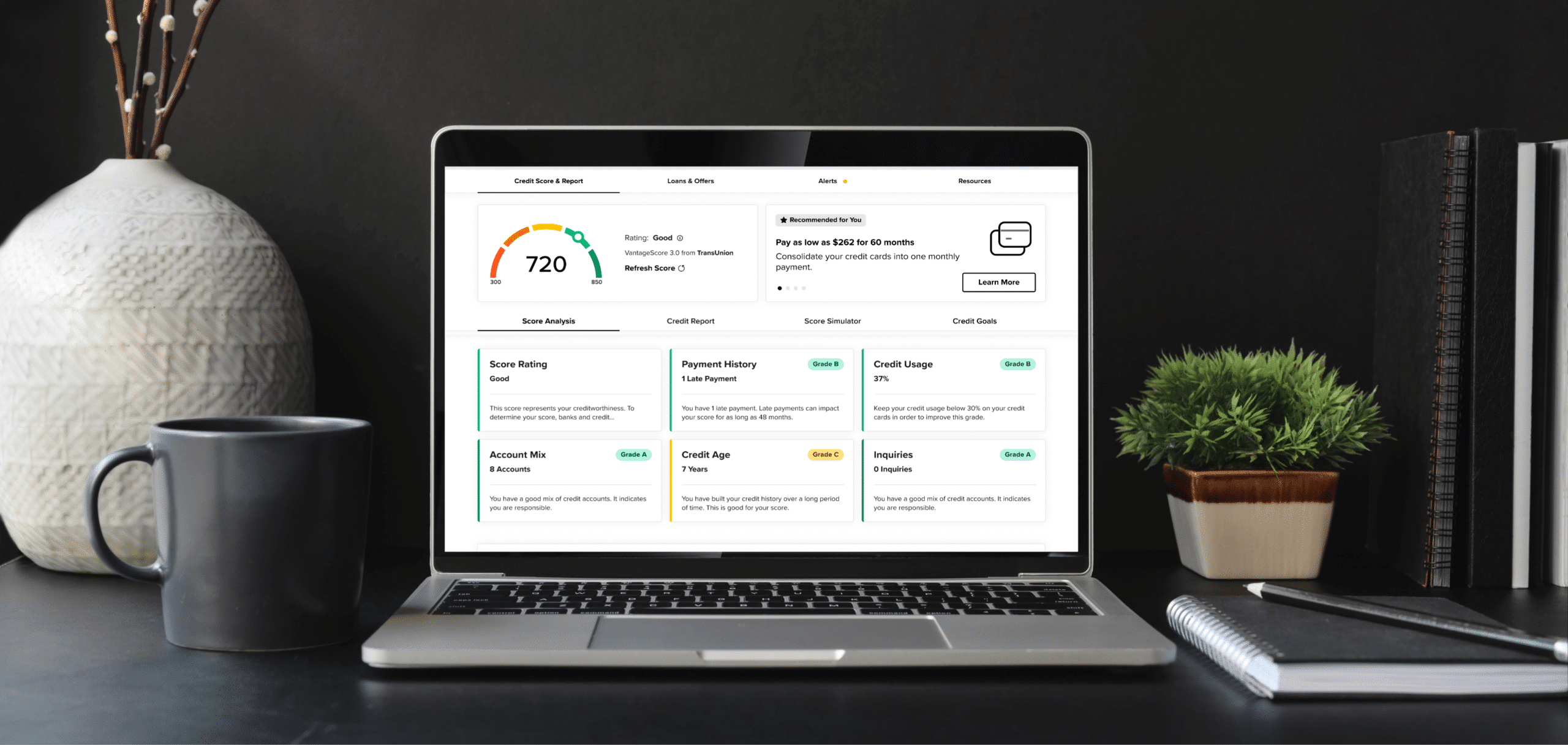

VantageScore, the company that generates the credit score you see here, uses five major categories of information, all of which were reported to the credit bureaus by your lenders to generate scores that range from 350 to 850 (higher is better, of course).

VantageScore Breakdown

Each category is weighed differently. Here’s how your VantageScore* breaks down:

- 40% Payment History. Lenders want to see a history of consistent, on-time payments.

- 23% Credit Usage. Also known as credit utilization, it’s the ratio between the total balance you owe and your total credit limit on your accounts.

- Tip: Try to keep your credit utilization at 30 percent or below. If you are consistently maxing out your credit cards, it may look like a sign of desperation in the eyes of a lender.

- 21% Credit Age. This is the age and type of credit you have. This percentage factors into how long you’ve had different kinds of credit accounts open. The older your credit history, the better.

- 11% Account Mix. Your credit account mix considers the number and type of accounts you have. Your score may be higher if you have a mix of both installment credit, like mortgages or car loans, and revolving credit, like credit cards.

- 5% Inquiries. This is based on recent credit applications. Opening multiple credit accounts in a short period could represent a greater risk for lenders — multiple recent inquiries may worry the lenders that you are applying to so many places because you are unable to qualify for credit — or because you need money in a pinch — so avoid opening too many accounts too quickly.

- Tip: You don’t have to worry about this if you’re shopping for a mortgage or car loan. All inquiries within 14 days count as a single inquiry.

How to Raise Your Score

Here are some easy-to-follow ways to boost your score.

Pull Your Credit Reports

You can pull your report from the three major credit scoring bureaus:

- TransUnion, Equifax, and Experian will each allow you one free copy of your report each week.

- If your financial institution is a SavvyMoney partner, you have access to your report and score daily through online or mobile banking.

- If you get a copy directly from the credit scoring bureaus, it’s a good idea to spread them out by pulling one every four months.

What to Do About Errors on Credit Reports

Once you’ve got your full credit report:

- Search for errors. If you find an error in your report, you should dispute it.

- Report errors immediately. Simple mistakes – the wrong address or a misspelling of your name – can be fixed by calling the creditor and asking for an update.

- Contact bureaus. If they won’t oblige or the error is more complicated, you should dispute directly with the credit bureaus. You can do this online.

Pay Your Bills On Time

One day late is still considered late, and just one late payment can lower your score.

Pay Down Credit Card Debt

You don’t want to use more than 30% of the total credit available to you. Keeping your utilization well below that (closer to 10%) can give your score a boost.

Hang Onto Old Cards

Your credit score benefits from long relationships with lenders, so cut them up, but don’t cancel them if you can help it.

Be Thoughtful About New Credit

Every time you apply for a new card or loan, the lender takes a peek at your credit history, which may ding your score.

Spread Your Debts Around

The mix of credit you have in your file—mortgages, student loans, auto loans, credit cards—shows that you can manage debt from multiple sources.

Patience

Remember that time and patience are key. You shouldn’t expect a change overnight, but you may see improvement in 12 to 18 months – shorter, if your score is already fairly high and you’re just looking for a bit of a bump.

*based on VantageScore 3.0